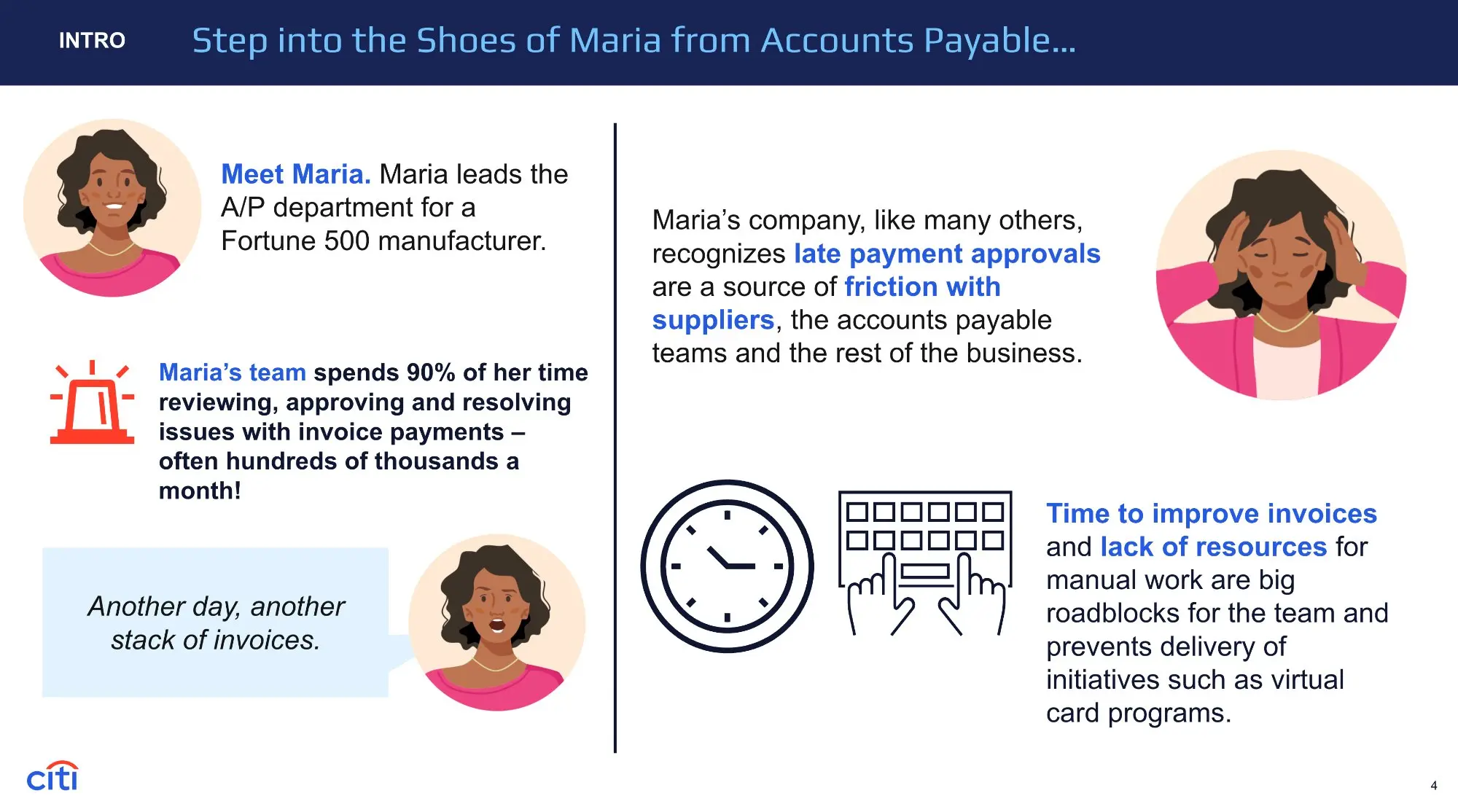

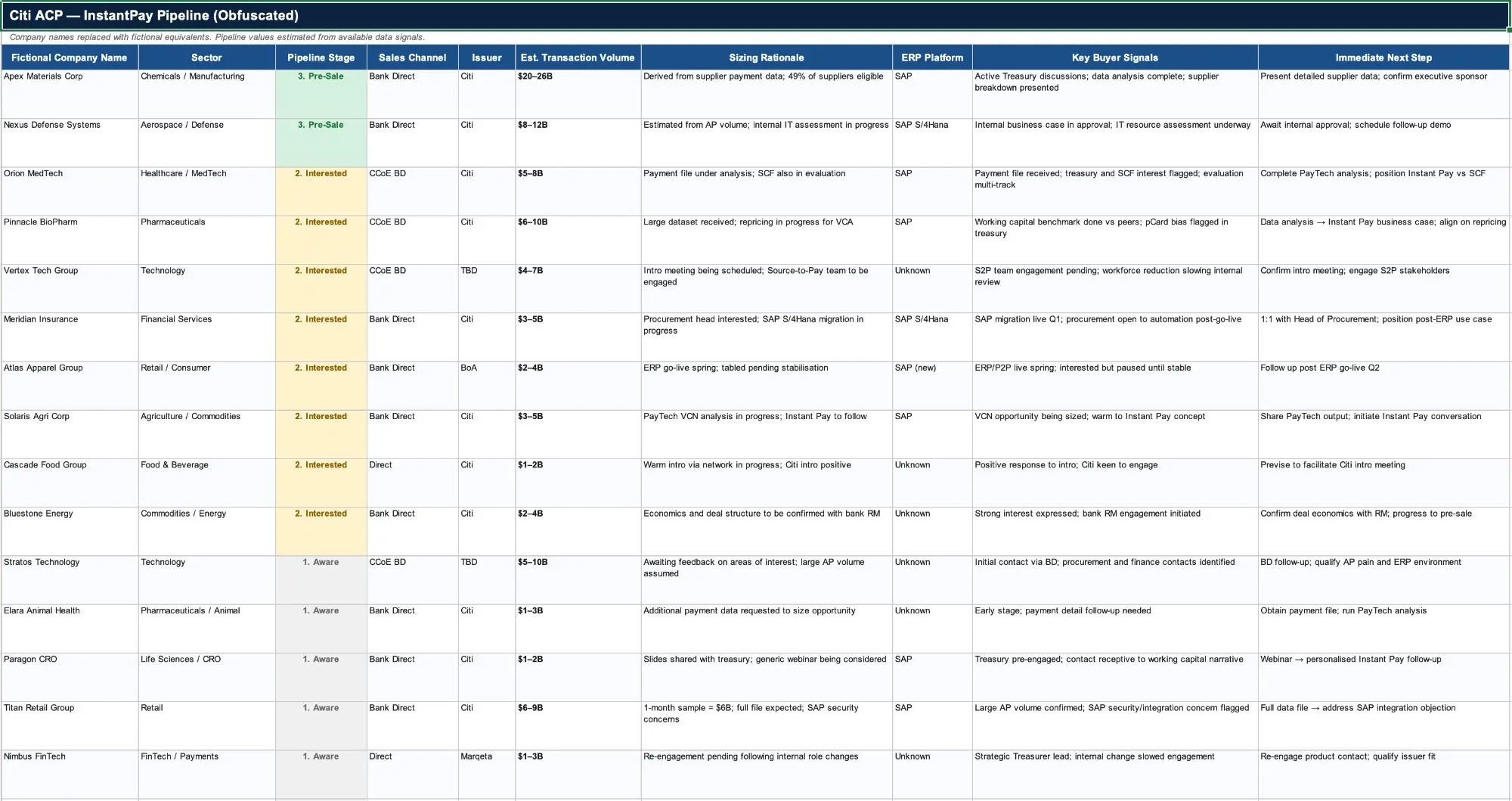

Lay the groundwork before activating the channel

Before a single sales conversation could happen, three things needed to be in place: a clear picture of who the right enterprise client was, a thorough understanding of how the Mastercard distribution team operated, and a live pilot that could prove the model with real results.